A&D Holon Holdings Deepdive

Description

A&D Holon Holdings is an off-the-radar Japanese precision instrument company that produces a critical semiconductor production tool which is transforming the company's profitability. Given the high relative growth and profitability of the company's semiconductor division, we expect consolidated operating margins to improve and drive c.50% earnings growth over the next two years. The company is significantly undervalued, trading at only 8x P/E, 6x EV/EBIT, and 1.3x P/B on FY Mar-2024 estimates, thus making for a potential investing opportunity.

Background:

A&D Holon Holdings (“A&DHH”) is a precision instrument manufacturer listed in Japan with a $350 million market cap and $450 million of sales. A&DHH was formed on 3/30/2022 through a merger of A&D Co and Holon Co, two listed Japanese companies. A&DHH specializes in industrial measuring and weighing equipment, medical and healthcare equipment, and semiconductor production and testing equipment.

A&D Co, the predecessor company, was founded in 1977 by several co-founders who previously worked at Advantest. One of the co-founders, Yasunobu Morishima, remains the President and Chairman of A&DHH. A&D stands for “Analog & Digital” and in the President and co-founder’s own words, “The company’s DNA is weighing and measuring technology.” A&D Co’s first two flagship products launched after its founding were electronic industrial scales and blood pressure monitors, which form the core of two of A&DHH’s three divisions. Since its founding, A&D Co has also produced Digital/Analog converters for electron beam lithography equipment, primarily to mask manufacturing equipment makers. A&D Co launched electron guns, beam deflection circuits that control the direction of electron beams, and high-precision D/A converters for electron beam lithography (DACs). A&D Co listed in Japan in April 2003.

Holon was founded in 1985 as a maker of devices for small-scale measurements using electron beams, and the company IPOed in Japan in February 2005 under the ticker 7748 JP. In recent years Holon’s main product has been CD-SEMs (critical dimension scanning electron microscopes). A&D Co and Holon had close ties from the beginning with A&D Co taking an 8.1% stake prior to the IPO. A&D Co then gradually raised its ownership by increasing its stake to 30.6% in March 2008, 51% in June 2018, and then finally 100% in March 2022 through a tender offer for all remaining Holon shares.

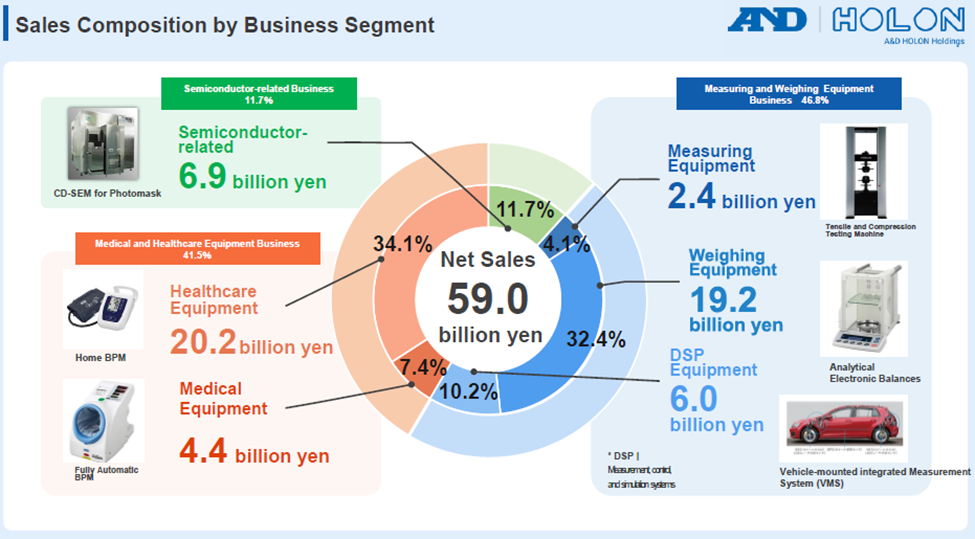

Business Segments:

A&D has three business segments. This slide from the company’s FY Mar-23 results briefing provides a good visualization of the sales composition.

Measuring & Weighing Equipment Segment (M&W) – 47% of sales and 26% of OP in FY Mar-2023:

The M&W business has #1 market share in Japan and #3 market share globally. M&W products include measurement devices for sound, vibration, material tensile strength, material thickness; weighing scales and sensors, metal and x-ray detectors; digital testing systems for EV batteries, and motor testing simulation software for auto manufacturers. Divisional sales are 69% weighing equipment, 22% DSP Equipment, and 9% measuring equipment. 59% of M&W sales are in Japan, 20% in the Americas, and 18% in Asia/Oceania.

The M&W division is a cash cow business with top domestic market share. Historical growth has been modest with sales growing at a 3.3% CAGR and OP growing at a 12% CAGR over the past decade. M&W operating margins have been steadily improving, reaching a record 9.2% last fiscal year. The M&W division is cyclical, and sales and operating profit contracted by -5% and -56% y/y during the past six months. We expect this division to perform in-line with this historical trend over the medium-term. However, management believes that a new EV testing business in the DSP subsegment could provide some upside relative to the division’s historical growth.

Medical & Healthcare Equipment Segment (M&H) – 42% of sales and 48% of OP in FY Mar-2023:

The M&H segment is predominantly focused on selling home-use blood pressure monitors and scales through pharmacies and big box retailers (82% of segment sales). The segment has c.10% global market share in home-use blood pressure monitors, which is second only to Omron, a Japanese competitor. The M&H division also includes a smaller subsegment that sells professional grade blood pressure monitors, scales, and software systems to hospitals and laboratories. The Americas and Europe each account for 38% of segment sales while Japan accounts for 22% of sales. Over the past decade, sales grew at a 5.5% CAGR and operating profit grew at a 9.4% CAGR with relatively limited cyclicality. Operating margin has averaged 20% post-Covid. Interestingly, management mentioned that they historically spent a lot on attending most global trade shows, but during post-Covid they realized that they can be more selective. As a result, they believe the current 20% operating margin is sustainable. M&H sales declined slightly y/y in the past 6 months due to a decline in blood pressure monitor orders from large customers, but profit grew by 12% y/y due to reduced shipping costs. We expect the M&H segment to grow top and bottom line at mid- to high-single digits over the medium-term.

Semiconductor Production Equipment Segment (SPE) – 12% of sales and 24% of OP in FY Mar-2023:

The SPE segment is comprised of two businesses, split between the A&D Co and Holon semiconductor equipment brands. The A&D Co business, which accounts for c.25% of segment sales, sells analog/digital and digital/analog converters (DACs) for single beam and multi beam mask writers used in the lithography process. The mask writer industry is dominated by three companies: JEOL (6951 JP), NuFlare (owned by Toshiba), and IMS (controlled by Intel). A&D supplies DACs for single and multi-beam writers to JEOL and NuFlare, while IMS manufactures their own DACs.

The Holon business represents the remaining c.75% of division sales. Holon has a 50% global market share in Critical Dimension Scanning Electron Microscopes (CD-SEMs) used in photomask lithography inspection. They compete with Advantest (6857 JP), which has the other half of the market. Our research also suggests that Holon also has 90%+ market share in photomask CD-SEMs within TSMC, the dominant company investing in leading node EUV technology. It is worth noting that Holon’s CD-SEM’s are not small, desk-based laboratory electron microscopes. They are very large, high-tech devices that we estimate are sold for multiple millions of dollars each. The picture below helps to put the size of the Holon CD-SEM into perspective.

CD-SEMs are also used in wafer processing, a segment of the market that requires different technology and a market in which Holon does not currently participate in. Hitachi High Technologies has c.80% market share in wafer CD-SEM.

The SPE segment is growing rapidly, with a 3-year sales CAGR of +42%. This growth is being driven by significant investment in EUV mask writers for leading node semiconductor fabs. The SPE segment accounted for 8% of consolidated sales in FY Mar-21 but this jumped to 19% of sales in the past 6 months. A&DHH’s SPE orders are also growing rapidly. While segment sales grew +36% y/y to JPY 6.9 billion in FY Mar-23, the reported order book grew by +72% y/y to JPY 11.9 billion. SPE sales in the first half of FY Mar-24 were JPY 5.6 billion, which is more than 80% of last year’s full year sales. While management does not disclose the quarterly order backlog, we understand that all of the sales filled year-to-date from the backlog have been replaced with additional orders.

Due to the oligopolistic nature of the CD-SEM and DAC markets, the divisional operating margin is more than 30%. In the most recent quarter, the operating margin hit a record high 41%.

Investment Thesis

We believe the market does not fully appreciate the financial contribution and competitiveness of A&DHH’s SPE segment. Holon’s CD-SEM product is a critical tool used in leading edge lithography and its profitability is materially improving A&DHH’s consolidated sales trajectory, profitability, and return on capital. We believe the Semiconductor division may account for nearly 50% of consolidated operating profit within 2 years. At 8x P/E, 6x EV/EBIT, 1.3x P/B, and 17% ROE, A&DHH is arguably the most undervalued leading edge semiconductor tool maker in the world.

We have conducted numerous interviews with industry experts, including A&DHH management, CD-SEM fab engineers, EUV mask R&D executives, and EUV mask lithography executives. Our findings suggest that the growth outlook for A&DHH’s SPE segment is very bright and underappreciated.

Demand for Holon photomask CD-SEMs is forecast to grow rapidly with more advanced lithography for multiple reasons.

-

Increased photomask layers (“mask counts”): As lithography shrinks from 7nm to 5nm to 3nm, the number of layers in a photomask that are below the “critical dimension” increases exponentially. Layers below this critical dimension require extra inspection time with a CD-SEM. For example, a 7nm photomask has about 5 layers, a 5nm mask has about 15 layers, and a 3nm mask has about 25 layers.

-

Mask yield improvement: TSMC’s 3nm photomask yields are estimated to be c.55% right now and the target is to increase yields to 90%. One way to improve mask yields is to increase the inspection frequency of the mask. Holon’s CD-SEM is highly evaluated by TSMC because the tool has very good software for aberration adjustment. Holon’s CD-SEM is used in conjunction with Lasertech and KLAC’s inspection tools. Lastertec’s inspection tool identifies the coordinates of the defect on the mask and Holon’s CD-SEM is used to inspect the defect.

-

EUV wafer production process: EUV is a much more technologically challenging than prior generation lithography processes. As a result, the EUV photomasks that pass final inspection to be used for wafer production need to be re-inspected periodically. This re-inspection was not required in older production methods like DUV or immersion. Our research suggests that an EUV mask needs to be re-inspected with a CD-SEM for every 250 wafers produced with the mask. Consequently, Holon’s CD-SEMs are required for both mask production and EUV wafer production.

-

Increasing Wafer Volumes for Advanced Node / AI Demand: Apple is currently the dominant end-customer for advanced node semiconductors, but demand is increasing rapidly from Nvidia and other GPU designers because of AI demand. Specifically, Nvidia’s AI Chip H100 is 5nm, the H200 is 4nm, and the D100 is 3nm. AMD and Intel are also aiming to enter the market for advanced AI chipsets by 2025, which may significantly increase demand for leading node technology. The trend is for these AI chips to be larger with smaller lithography, which results in accelerating chip photomask complexity that will require more CD-SEM inspection tools.

-

Entry into CD-SEM for wafer inspection: Management is planning to enter the CD-SEM market for wafer inspection in approximately 2 years. This is a much larger TAM market that is currently dominated by Hitachi High Tech and KLA-Tenor. While success is not guaranteed, if Holon is able to gain even a small share of this market it could add a significant additional leg of growth to the SPE segment.

One expert we spoke to estimates that the market for photomask CD-SEMs will grow by at least 50% in the next two years. We believe management is in the process of expanding its CD-SEM capacity to around 30 units up from approximately 20 units currently and only 10 units back in 2020. We believe these data points corroborate that A&DHH’s SPE segment growth will continue to be strong for at least the next two years.

Financials and Valuation

Below is a detailed table of historical financial data and our forecast through FY Mar-26. There are several observations worth highlighting:

-

Operating margins have been steadily improving in recent years and we expect this trend to continue as the high-margin SPE segment contributes a larger share of profits. The SPE segment may contribute nearly 50% of consolidated profits within two years.

-

This is an R&D focused company with annual R&D expenditure accounting for 8-12% of sales.

-

ROE has been steadily improving in recent years.

-

The business carries significant working capital, primarily in inventory, because they do not use distributors for any of their key segments. We believe this could be an area for improvement although we don’t have any indications that changes in working capital management are underway.

-

We expect the company to continue deleveraging and perhaps reach a net cash position in FY Mar-25 or Mar-26. This may allow management to consider increasing the dividend payout ratio and/or conduct share buybacks.

-

The current P/E and EV/EBIT valuation multiples are near decade lows despite the improving financials and compelling near-term growth opportunity in the SPE segment.

We believe A&DHH is significantly undervalued. The stock has traded at a 10-year average valuation of 12.5x EV/EBIT and 15.4x P/E. Applying these historical average multiples to our FY Mar-25 estimates suggests upside of between 108-133%. Our DCF analysis also implies upside in-line with these average historical multiples.

We have also analyzed comparable company multiples. Comps for each division trade at significantly higher EV/EBIT multiples (25-40x) and P/E multiples (40-50x). The peer companies are much larger than A&DHH, so a small cap discount may be justified. Nevertheless, A&DHH appears to have significant upside potential using any type of valuation analysis.

Management

A&DHH is led by Chairman and President, Mr. Morishima Yasunobu, the entrepreneurial co-founder of A&D Co. Mr. Yasunobu directly owns a 0.89% stake, and we understand that senior management collectively own c.10% of the company. We believe management has built a strong business with three segments, all of which have high market shares and leverage on the company’s strength in weighing and measurement technologies. They have an R&D centric culture, which is likely to drive future product launches and continued growth. While working capital management and shareholder return policies have some room for improvement, the company has nevertheless maintained a high teens ROE and double-digit profit growth over the cycle.

Risks

Cyclicality: The SPE industry is cyclical and Holon’s SPE business has suffered cyclical downturns in the past including 2005-08, 2013, 2016, and 2020. However, we believe that the EUV technology investment trend limits the likelihood of a cyclical downturn for CD-SEMs in the near-term. Moreover, management told us recently that although the semiconductor industry has been in a downturn during the past year, A&DHH’s SPE tools are used in the pre-production process and therefore demand has remained resilient. The M&E segment is also cyclical, but we don’t believe this segment poses much risk to our thesis given that the division is already in a modest cyclical downturn, and it only contributed 8% to group profit during the past 6 months.

Order Lumpiness: The CD-SEM is a high-ASP, low volume business (20-30 units per year). Although we have a high degree of conviction that the 2-year CD-SEM growth trend is strong, it is possible that quarterly SPE sales could be lumpy and sales might decline on a quarterly sequential basis depending on order delivery timing. This could cause share price volatility, particularly because the stock has limited sell-side coverage and the SPE orderbook is only announced on an annual basis.

Russia: Approximately 25% of the M&H segment revenue is from Russia. The company stopped selling all weighing and measuring products in Russia right after Russia attacked Ukraine in February 2022, but A&D still sells blood pressure monitors in Russia for humanitarian reasons. The company is still able to repatriate and convert rubles to Japanese yen via Japanese banks. Management is unlikely to exit the Russian blood pressure monitor business unless government sanctions require it or unless the Russian government uses nuclear weapons in the war. If management were forced to exit Russia entirely, we think the negative impact would be manageable at c.10% of revenue, c.15% of operating profit, and limited inventory impairment risk.

Currency: Management does not disclose FX sensitivity except to say that a weaker Japanese yen is generally favorable for earnings. 55% of sales are in Japan (including all SPE segment sales), 22% are to the Americas, 14% are to Europe (mostly Russia), and 9% are to Oceania (Australia and Korea are important countries in this segment). Many of the company’s raw material costs are denominated in USD so there is some natural hedging for movements in the USD vs. JPY.